On-Site PPAs - Will the planned changes to the German electricity tax exemption soon make them even more attractive?

Contacts

Counsel

Germany

Based in Frankfurt, I advise national and international clients with regard to German tax law.

Associate

Germany

As an associate, I am part of Bird & Bird's tax law practice based in the Frankfurt office. I advise national and international clients on German and international tax law.

On-site power purchase agreements (“On-Site PPAs”) have become increasingly important in recent years, particularly due to the growing demand for green energy and as a hedge against fluctuating electricity prices. These contracts enable companies to utilise electricity produced directly on site from renewable energy sources, which not only makes ecological sense but also offers financial benefits – for example by eliminating grid fees and electricity tax exemptions.

However, the current legal interpretation of the term “installation” for On-Site PPAs often leads to unexpected problems, particularly in relation to the electricity tax exemption. In this article, we shed light on how the current government draft for the modernisation of German electricity and energy tax law could remove such hurdles and what this means for the future of on-Site PPAs.

The market for Power Purchase Agreements (“PPA”)

PPAs are also becoming increasingly popular in Germany. According to the “PPA Market Analysis Germany 2023” by the German Energy Agency, the total volume of electricity supplied under PPAs has increased rapidly by 323 per cent compared to the previous year (2022).

This is hardly surprising, as the conclusion of a PPA is economically advantageous for both the electricity producer and the electricity consumer. A PPA usually stipulates that electricity must be purchased at a predetermined price over a period of up to 10 years. This provides a reliable source of income for the electricity producer, which facilitates the financing and realisation of projects if there are also reliable surpluses in relation to the electricity generation costs. They protect the electricity consumer from price fluctuations in electricity prices and make the electricity costs of operation more predictable.

The different forms of PPAs

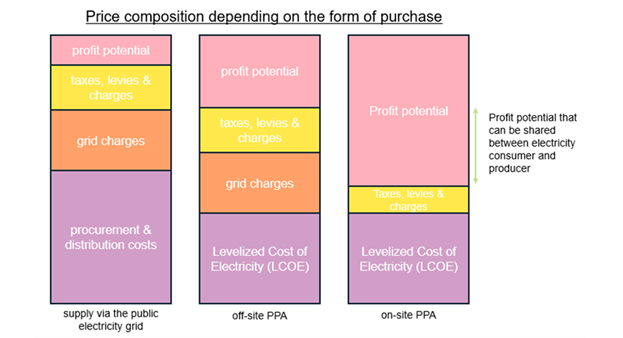

A distinction can be made between On-Site PPAs (electricity generated is produced directly at the end consumer's premises and supplied to them via a direct line) and off-site PPAs (electricity generated is supplied to the end consumer via the public electricity grid).

The type of PPA has a significant impact on the potential earnings opportunities. In this context, On-Site PPAs are particularly attractive because they generally do not incur any grid fees or grid-related levies and charges, as the public electricity grid is not utilised. There may also be an exemption from German electricity tax. The resulting benefit from the reduction in tax, levies and costs is usually split between the electricity producer and the electricity consumer. The special features of On-Site PPAs in terms of price composition and their impact on earnings potential are illustrated in the following chart:

German electricity tax exemption for On-Site PPAs - the current situation

But what determines whether an exemption from German electricity tax can be granted for On-Site PPA projects?

Pursuant to Sec. 9 para. 1 no. 3 lit. b) German Electricity Tax Act (“StromStG”, Stromsteuergesetz), electricity generated from renewable energy sources or in high-efficiency combined heat and power plants (KWK-Anlagen) with a rated electrical output of up to two megawatts and which is supplied by the person operating the plant or having it operated to end consumers who draw the electricity in the geographical vicinity of the plant is exempt from electricity tax.

The term “installation” used in the StromStG can lead to unintended consequences. This is understood broadly and can lead to installations that are not located at the same site being grouped together. As a result, this can have far-reaching consequences. If this so-called plant aggregation is not recognised, this can lead to the limit of two MW being unintentionally exceeded and thus to the refusal of the electricity tax exemption calculated in the profitability analysis. Due to its significance, the current definition of an installation is therefore described in detail below.

The term “installation” is not defined in the StromStG. In this respect, it must be interpreted independently and functionally. Strong indications for the existence of an overall installation are the spatial grouping of several units at one location (e.g. a building), operation by one operator and the supply of a specific customer group.

However, the provision of Sec. 12b para. 2 sent. 1 German electricity tax implementing ordinance (“StromStV”, Verordnung zur Durchführung des Stromsteuergesetzes) must also be used to interpret the definition of an installation. According to this, even electricity generation units at different locations are deemed to be one installation, provided that

- the individual power generation units are centrally controlled for the purpose of power generation and

- The electricity generated is to be at least partially fed into the supply grid.

According to Sec. 12b para. 2 sent. 1 no. 1 StromStV, centralised control is given if the individual electricity generation plants are controlled remotely in accordance with Sec. 20 no. 1 in conjunction with Sec. 10b para. 1 no. 2 lit. b of the German Renewable Energy Sources Act (“EEG”, Erneuerbare-Energien-Gesetz). Sec. 10b para. 1 no. 2 lit. b EEG in the current version (formerly Sec. 36 EEG in the version dated 21 July 2014). The wording presupposes that the individual electricity generation units are controlled for the purpose of generating electricity. However, according to the fiction of Sec. 12b para. 2 sent. 1 no. 1 half-sent. 2 StromStV, this is to be regarded as given under the conditions stated therein, without it being important that remote control takes place. Rather, according to the fiction of Sec. 12b para. 2 sent. 1 no. 1 half-sent. 2 StromStV, it is sufficient if the possibility of remote control exists.

In large-scale On-Site PPA projects between a supplier and a large industrial customer, this broad understanding has led to considerable difficulties, especially in cases where the electricity produced by the On-Site plants exceeds the industrial customer's electricity requirements. The surplus electricity must then be fed into the supply grid. To receive support under the EEG in the form of the market premium (Sec. 20 EEG) for this part of the electricity generated, the systems must be remotely controllable using technical equipment. In large-scale On-Site PPA projects across several locations of the electricity consumer or even different electricity consumers, this can mean that the tax exemption does not apply, as the nominal electrical output of up to two megawatts is exceeded due to the interlinking of the systems.

According to the current interpretation by the courts (see Düsseldorf tax court, judgement of 4 October 2023 - 4 K 1072/23 VSt, margin no. 25 and judgement of 21 February 2024 - 4 K 1324/22 VSt, margin no. 29), the exemption in Sec. 12 para. 3 sent. 2 StromStV cannot provide a remedy either (see comments by the German Retail Association HDE of 31 August 2023).

Until now, the only way to counteract this was to create different operators for the respective locations by interposing companies to prevent a clustering of plants or at least to ensure that no more plants with a nominal electrical output of less than two megawatts were counted together per company.

As regards bracketing, it was also particularly unsatisfactory that the main customs offices only applied this system unilaterally to the detriment of the taxpayers. While it was possible to fall out of the tax exemption according to Sec. 9 para. 1 no. 3 lit. a StromStG due to the system bracketing, this was not applied for the tax exemption according to Sec. 9 para. 1 no. 1 StromStG, according to which a nominal output of at least 2 MW would be required. This result is hardly comprehensible and could be one of the reasons for the subsequent amendment.

Improvement in sight? New draft law gives hope!

The (proposed) Act on the Modernisation and Reduction of Bureaucracy in German Electricity and Energy Tax Law (the “New Law”) is intended to comprehensively adapt and modernise electricity and energy tax law to current developments and reduce bureaucracy at the same time. The government draft of the New Law has also been available since 15 May 2024.

Among other things, it provides for the abolition of the system bracketing for decentralised electricity generation and for the assessment of tax exemptions to be uniformly based on the location of the respective electricity generation system in future (p. 1 of the New Law draft). The conditions on site will then be decisive for determining the size of an electricity generation plant. The remote controllability of electricity generation plants should therefore no longer lead to the aggregation of the plant output and, if applicable, the exclusion of the electricity tax exemption pursuant to Sec. 9 para. 1 no. 3 lit. b StromStG (p. 46 of the New Law draft).

It would be welcome if this provision were to be included in the proposed legislation, as this would result in a noticeable improvement in practice and unnecessary administrative work for companies could be avoided.

Update from 7 January 2025: On 16 October 2024, the Finance Committee presented its recommendation on the German government's draft bill, on the basis of which the bill was to be passed by the Bundestag on 18 October 2024. The planned changes discussed in this article were not affected.

Unfortunately, at the request of a member of the Bundestag, the Bundestag was declared to be quorate on 18 October 2024. On the actual replacement date, 7 November 2024, the bill was dropped due to the break-up of the traffic light coalition.

Since the bill was not passed in 2024, it is unlikely to be passed after the end of the traffic light coalition until the new elections on 21 February. The bill is thus in danger of falling victim to the discontinuity of the Bundestag.

Update from 5 November 2025: After the previous draft did not pass the legislative process, the change described in the article is now included in the draft bill for the Third Act Amending the Energy Tax and Electricity Tax Act of 29 September 2025. We'll keep you updated on how the new draft is progressing.

{kind=link}