Real Estate Transfer Tax without an own transaction: Tax pitfalls in share buy-backs

Contacts

The Federal Fiscal Court (Bundesfinanzhof, "BFH") has, by ruling dated 22 October 2025 (II R 24/22), continued its case law on the consolidation of shareholdings in connection with the acquisition of own shares:

Where a real-property-owning limited liability company ("GmbH") acquires its own shares and, as a result, the interest of a shareholder — without taking into account the shares held by the company itself — mathematically increases to at least 95%, the statutory condition for a consolidation of shareholdings (Anteilsvereinigung) pursuant to Sec. 1 para. 3 no. 1 or no. 2 of the Real Estate Transfer Tax Act "GrEStG") in the version applicable in the dispute year 2010 is fulfilled. This applies even where several shareholders hold the shares not held by the company itself (continuation of the BFH ruling of 20 January 2015 — II R 8/13, BFHE 248, 252, BStBl II 2015, 553).

A notification […] does not have the effect of terminating the commencement-blocking period under Sec. 170 para. 2 sent. 1 no. 1 of the General Tax Code ("AO") with regard to the assessment limitation period, where the particulars required under Sec. 20 para. 1 nos. 2 and 3 GrEStG in relation to the properties are entirely absent.

The case illustrates in a highly instructive manner how quickly share buy-backs can give rise to substantial real estate transfer tax liabilities, and what pitfalls lie in wait in connection with the notification obligation. Market participants would do well to keep this in mind.

1. Facts: Share Buy-Back Involving a Real-Property-Owning Company

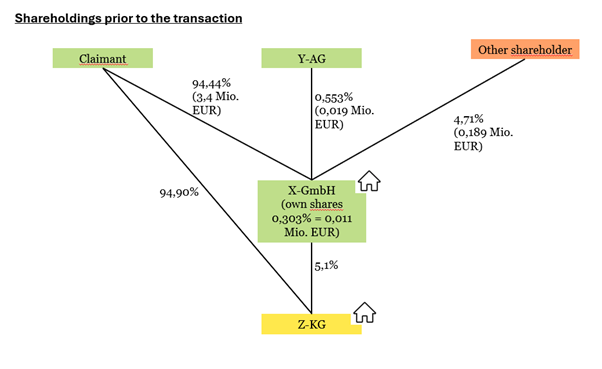

The ruling was based on a multi-tier ownership structure in which the claimant held both a direct interest in a real-property-owning limited partnership (Kommanditgesellschaft, "KG") and an indirect interest through a real-property-owning GmbH.

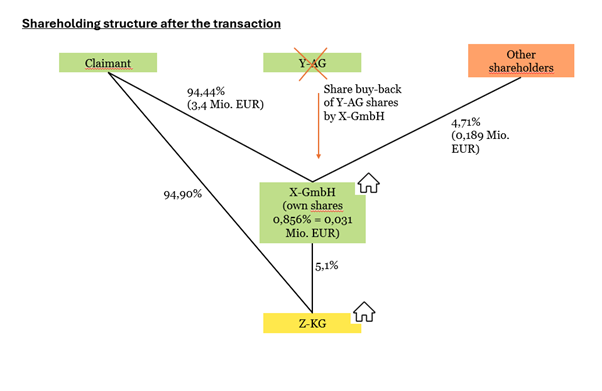

By notarised agreement dated 26 January 2010, Y-AG sold its shareholding in X-GmbH, amounting to 0.553%, to X-GmbH itself. As a result, the holding of own shares by X-GmbH increased to a total of 0.856%.

The notary had, by letter dated 27 January 2010, forwarded a certified and a simple copy of the notarial deed to the tax office. The claimant itself had not filed a notification. It was not until 25 April 2016 that a letter from the claimant, designated as a notification pursuant to Secs. 19, 20 GrEStG, reached the tax office, in which the claimant indicated that the acquisition of the shares by X-GmbH might have given rise to a consolidation of shareholdings.

By assessment dated 21 November 2017, the tax office assessed real estate transfer tax against the claimant in respect of a consolidation of shareholdings arising from the agreement of 26 January 2010.

The Fiscal Court ("FG") Münster dismissed the action brought against this assessment. It found that, as a result of the acquisition of own shares, the shares in X-GmbH and in Z-KG had been consolidated — directly and indirectly — in the hands of the claimant for the purposes of real estate transfer tax. Furthermore, at the time of issuance of the first real estate transfer tax assessment on 21 November 2017, the assessment limitation period had not yet expired. The claimant subsequently lodged an appeal on points of law (Revision) with the BFH.

2. Decision: Own Shares Are Disregarded

The BFH dismissed the claimant's appeal and confirmed the FG's decision that, as a result of the acquisition of own shares by X-GmbH, the shares in that company and in Z-KG had been consolidated — directly and indirectly — in the hands of the claimant for the purposes of real estate transfer tax within the meaning of Sec. 1 para. 3 no. 1 or no. 2 GrEStG.

As its central finding, the court held that, when examining whether the 95% threshold for a direct or indirect consolidation of shareholdings has been reached, own shares held by a corporation acting as an intermediate company or as a real-property-owning company must be disregarded (marginal nos. 17 et seq.).

Accordingly, the acquisition of its own shares by X-GmbH fulfilled the statutory condition for a consolidation of shareholdings in the person of the claimant pursuant to Sec. 1 para. 3 no. 1 or no. 2 GrEStG. This also applies where several shareholders hold the remaining shares not held by the company itself (marginal no. 18, continuing the BFH ruling of 20 January 2015 — II R 8/13, BStBl II 2015, 553).

In the hands of the claimant, at least 95% of the shares in X-GmbH had been consolidated, and accordingly the statutory condition of Sec. 1 para. 3 GrEStG was fulfilled (marginal no. 20). By virtue of the notarised agreement of 26 January 2010, X-GmbH had acquired own shares with a nominal value of EUR 19,920 from Y-AG. Following the transaction, X-GmbH held a total of EUR 30,840 in its own share capital of EUR 3,600,000. Since the shares held by X-GmbH in itself are not to be taken into account when calculating the relevant percentage, the claimant's interest in X-GmbH mathematically increased to 95.26% (EUR 3,400,000 out of EUR 3,569,160).

A partly direct, partly indirect consolidation of shareholdings in the claimant also occurred with respect to the properties belonging to Z-KG (marginal no. 21). Prior to the acquisition of its own shares by X-GmbH, the claimant held a direct 94.9% interest in Z-KG as a limited partner. As its interest in X-GmbH increased to 95.26%, X-GmbH's limited partnership interest of 5.1% was also attributable to the claimant (cf. BFH ruling of 27 May 2020 — II R 45/17, marginal nos. 18 et seq.), such that the claimant held at least 95% in the KG.

3. Requirements for a Complete Notification

The court found that a notification does not have the effect of terminating the commencement-blocking period under Sec. 170 para. 2 sent. 1 no. 1 AO with regard to the assessment limitation period where the particulars required under Sec. 20 para. 1 nos. 2 and 3 GrEStG in relation to the properties are entirely absent. The notification must contain a description of each individual property by reference to the land register, cadastre, street and house number, as well as the size and type of development. Obtaining these particulars within the notification period is often difficult in practice.

The notary's letter of 27 January 2010 did not satisfy these requirements. Neither the notarial deed nor the covering letter identified the properties affected by the acquisition. For want of a valid notification pursuant to Sec. 170 para. 2 sent. 1 no. 1 AO, the four-year assessment limitation period only began to run at the end of the third calendar year following the accrual of the tax — i.e., at the end of 2013 — and did not expire until after issuance of the first real estate transfer tax assessment on 31 December 2017.

4. Income Tax Aspects of the Buy-Back of Own Shares

Following the introduction of Sec. 272 para. 1a sent. 1 of the Commercial Code ("HGB") by the Accounting Law Modernisation Act ("BilMoG"), the accounting treatment of own shares in the company's tax balance sheet remains contentious.

With regard to the treatment at the level of the (former) shareholder transferring the shares to the company, it is settled that this constitutes a disposal that may fall within the scope of Sec. 17 of the Income Tax Act ("EStG"). The case of a partition in kind of commercial partnerships has likewise been decided (BFH, rulings of 21 August 2025 — IV R 15/22 and IV R 16/22). Where own shares are acquired from a shareholder above their market value, or disposed of to a shareholder below market value, this may additionally trigger a hidden profit distribution at shareholder level (BFH, ruling of 13 May 2025 — VIII B 33/24; see also Federal Ministry of Finance ("BMF") circular of 27 November 2013 — IV C 2 – S 2742/07/10009).

The real estate transfer tax consequences of own shares for the purposes of the percentage calculation also apply to income tax under Sec. 17 EStG: own shares are likewise not to be taken into account, for example, when determining the relevant shareholding percentage (BFH, ruling of 5 April 2022 — IX R 19/20).

5. Recommendations

The buy-back of own shares by real-property-owning companies carries real estate transfer tax risks that are frequently overlooked in practice. The critical factor is that own shares are not taken into account when calculating the 90% threshold, with the result that the remaining shareholders mathematically reach higher ownership percentages. This can trigger a consolidation of shareholdings without any actual change in the shareholders' ownership interests. Particular caution is therefore warranted.

Especially problematic is the fact that notification obligations are frequently also misjudged in such cases, which leads to the tax authorities drawing the real estate transfer tax consequences even years later.

In addition, income tax and gift tax consequences must also be kept in mind.

Through early tax law advice in connection with share transactions and restructurings, these risks can be identified and minimized in good time. We would be happy to advise you in this regard.

***

The foregoing remarks are provided for information purposes only and do not constitute legal or tax advice

{kind=link}